What is a car lease Money factor?

Money Factor Explained: What It Means and Why It Matters When Leasing a Car

When you’re leasing a vehicle, it’s easy to focus on monthly payments and ignore the finer details in the lease agreement. But one small number buried in the fine print can have a big impact on what you ultimately pay: the money factor. If you’ve ever seen a figure like .00125 on a lease contract and had no idea what it meant, you’re not alone. In this article, I’ll walk you through what the money factor is, how to convert it to an interest rate, and why understanding it can save you thousands over the life of your lease.

What Is the Money Factor in a Car Lease?

The money factor is essentially the lease equivalent of an interest rate. While traditional auto loans use an APR (annual percentage rate), leases use this decimal figure to represent the cost of financing the vehicle over the lease term.

Dealers and leasing companies use the money factor to calculate the finance charge—this is the portion of your lease payment that covers the cost of borrowing the car. A lower factor means less interest paid over time, while a higher one increases your overall expense. Even a seemingly small difference in the number can significantly affect your monthly payment.

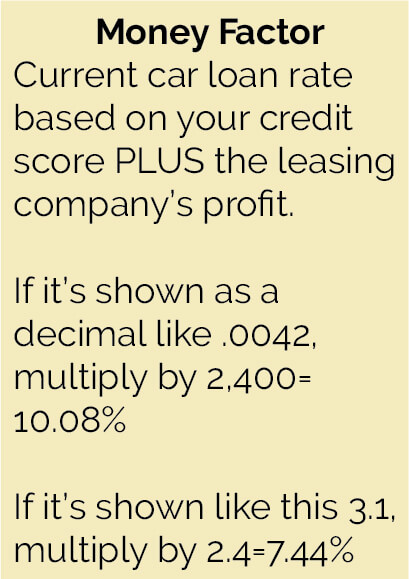

How to Convert Money Factor to an APR

One of the most common questions I get is: “How do I know if the money factor is fair?” To evaluate it properly, you’ll want to convert it into a more familiar APR.

Here’s the simple formula:

Money Factor × 2,400 = APR

For example:

0.00125 × 2400 = 3.0% APR

0.00200 × 2400 = 4.8% APR

Once you know how to do this conversion, you can directly compare lease costs with standard auto loans—and better yet, you can negotiate more confidently. Some dealerships inflate the base figure to increase their profit margins, which is why it’s so important to understand this component of your lease.

Where to Find It in the Paperwork

Unfortunately, the money factor isn’t always front and center on lease documents. You may need to specifically ask your dealer what it is. If they won’t tell you or dodge the question, consider that a red flag.

Sometimes, it’s displayed with multiple decimal places—like .00215—which can look insignificant at first glance. But don’t be fooled. A difference of just .00040 can add hundreds of dollars to your lease over a 36-month period.

How the Money Factor Affects Your Monthly Lease Payment

Your monthly lease payment is made up of three key components:

• Depreciation – the reduction in the car’s value during your lease term.

• Taxes and fees – based on your local jurisdiction.

• Finance charge – determined by the money factor.

Even if you negotiate a low sale price, a high money factor can still make your lease more expensive. Let’s look at an example.

MSRP: $35,000

Negotiated price: $33,000

Residual value (end of lease): $20,000

Lease term: 36 months

Money factor: 0.00200

The finance charge is calculated like this:

(33,000 + 20,000) × 0.00200 = $106/month

If you instead qualify for a rate of 0.00150, the charge drops to:

(33,000 + 20,000) × 0.00150 = $79.50/month

Over the life of the lease, that’s nearly $950 in savings—just from negotiating a better money factor.

Can You Negotiate the Money Factor?

Sometimes you can, and you absolutely should try. Leasing companies set a base money factor, also known as the buy rate, but dealerships are often allowed to mark it up. If you have excellent credit, you likely qualify for the best rates. But unless you ask, you might get quoted a marked-up version designed to boost the dealer’s profit.

If the dealer won’t reduce it, try negotiating the vehicle’s selling price instead. Both the sale price and money factor affect your monthly cost, and either one can tip the scale in your favor.

Credit Score and the Money Factor

Your credit score plays a major role in determining what money factor you’ll be offered. Just like with loans, the best lease terms are reserved for high credit scores—typically 720 and above. If your score falls below that range, expect a higher factor and a more expensive lease overall.

It’s a good idea to check your credit score and get pre-approved for a lease through a bank or credit union before you walk into the dealership. That way, you’ll know what factor you should realistically expect.

©, 2016 Rick Muscoplat

Posted on by Rick Muscoplat